Tax incentives and skills: A cautionary tale about the risk of complexity

By Stijn Broecke.

“The hardest thing in the world to understand is the income tax.” –Albert Einstein.

Tax incentives are used widely across OECD countries to incentivise individuals to invest in post-compulsory education and training – however little is known about their effectiveness. Recent evidence from the United States highlights the risk of creating overly complex systems in which the embedded incentives are no longer fully understood by individuals. This carries an important lesson for other countries in designing their own tax measures for skills investments.

Tax incentives are widely used to nudge people into acquiring skills

While there are many reasons why individuals invest in education and training, an important motivation is the expected return in terms of higher future earnings in the labour market. In fact, the high returns attached to most forms of education and training have been used by many governments across the OECD to move towards a higher degree of cost sharing between the state and the individual, and towards a greater role for the market in determining education and training investments.

However, it is not clear that individuals (and young people in particular) always fully understand the benefits of an investment in education and training. For example, they might be risk averse or short-sighted and therefore under-value the future stream of benefits that could flow from what seems to be an initially costly investment in skills. In addition, individuals will only really take into account the benefits to themselves of such investments, and ignore the wider benefits to society – such as better health, greater civic engagement and lower benefit dependency.

These are just two reasons why, if left to the market, the level of skills acquired by individuals is likely to be sub-optimal from society’s point of view. This is also why, despite allowing a greater role for the market in determining education and training choices, governments will continue to play an important role in making sure that the supply of skills is closely aligned to the demand.

However, this role has become more indirect than before and increasingly consists in ‘steering’ the system and ‘nudging’ individuals and firms into acquiring the right quantity and type of skills, rather than attempting detailed planning in the allocation of individuals to courses. One way in which governments can do this is by implementing policies that alter the costs and future benefits of investments in education and training, and they have a wide variety of tools at their disposal that allow them to do so – one of which is the tax system.

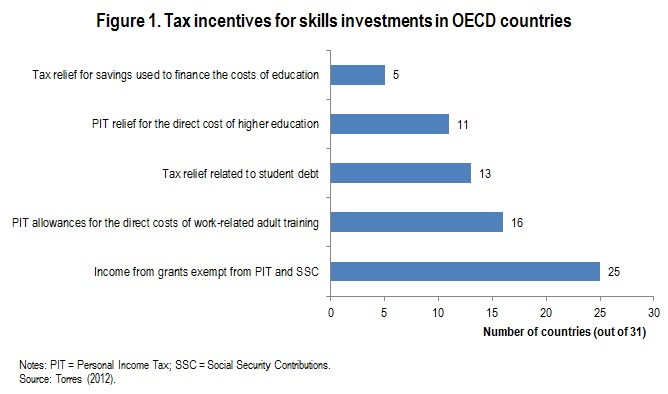

A 2012 OECD working paper showed that tax measures to incentivise individuals to invest in education and training are widely used across the OECD (Figure 1), and include personal income tax (PIT) relief and reductions in social security contributions (SSC) for education-related expenses, as well as tax relief for savings used to finance the costs of education. It is important to point out that such measures are used primarily for post-compulsory education, where there is the biggest role for cost sharing and financial incentives

But recent evidence from the United States suggests that they should be used carefully

One country where tax measures are widely used is the United States. For example, in 2015, households received USD 19.7 billion in tax credits for education, and these tax credits (like the American Opportunity Tax Credit) are just one of more than a dozen different tax subsidies available. Families of future college students benefit from tax-advantaged savings plans, like the Coverdell and 529 programmes. Current college students and their families benefit from: deductions for tuition costs and loan interest; exclusion of scholarships, grants and tuition fee from taxable income; and a dependent exemption for students aged 19 to 23. And graduates receive subsidies in the form of tax deductions for interest paid on student loans.

However, a recent NBER working paper by Dynarski and Scott-Clayton (2016) argues that “the increasing scope and diversity of [tax] subsidies implies increased complexity” and that, as a result, families often fail to make optimal choices as many do not fully understand the eligibility rules and benefit calculations, and how they interact with other elements in the tax system. The authors cite estimates by the United States Government Accountability Office which suggest that around 14% of families eligible for an education tax benefit failed to claim it, while 40% of filers who used the tuition tax deduction would have been better off claiming one of the tax credits.

Dynarski and Scott-Clayton (2016) also argue that there is “compelling evidence” that the tax incentives in the United States have “zero effect on human capital accumulation”. In particular, they cite two recent studies by Bulman and Hoxby (2015) and Hoxby and Bulman (2016) that use administrative data from the Internal Revenue Service and employ regression discontinuity and difference-in-differences methods to show that neither the Hope Tax Credit (the precursor of the AOTC), nor the Tax Credit for Lifelong Learning (TCLL), nor the American Opportunity Tax Credit have any effect on enrolment in education.

In addition to the complexity of the system, the authors argue that a key problem with tax incentives is that they are not pocketed by the beneficiaries until nearly one year after enrolment decisions are made – which could be a significant problem for cash-constrained individuals in particular. The fact that most tax incentives appear to benefit primarily middle- and high-income households leads the authors to argue for reforms which would: (i) target the incentives more on those households whose investments are most price-sensitive, and (ii) deliver them at the point when education expenditures are made.

A final explanation for why tax incentives may have little effect on educational enrolment in the United States is that institutions are capturing some of these tax benefits via increases in fees or reductions in financial aid. For example, Long (2004) found that tax relief led to faster tuition growth in certain educational institutions, while Turner (2012) argued that institutions reduced their own sources of grant aid.

Tax incentives for skills investments: Where to now?

The Dynarski and Scott-Clayton (2016) study does not necessarily mean that tax incentives should not be used as a policy tool to get individuals to invest in education and training. However, it does tell a cautionary tale about the risks of complexity, and countries using such measures should therefore think carefully about the design of their tax incentives – including how they interact with the rest of the tax system and other measures aimed at encouraging skills acquisition. Another lesson to take away is that, apart from a few studies in the United States, we know next to nothing about the effectiveness of tax measures in promoting education and training – despite the fact that such measures are widely used across the OECD. More research into this area is therefore an important priority for future research.